🔎 How do I find the Certainty Equivalent?

This page illustrates a five-step process that you will need to use to solve three classes of problems:

- you have to calculate the EU of something and are given a diagram, but don’t have enough information to solve it using a calculator and the formula for EU.\

- you have to calculate the Certainty Equivalent that someone will pay given a risky situation that they face.

- you have to calculate the maximum premium that someone will pay given a risky situation that they face.

Given that many questions like this will pop up, it is a very useful page!

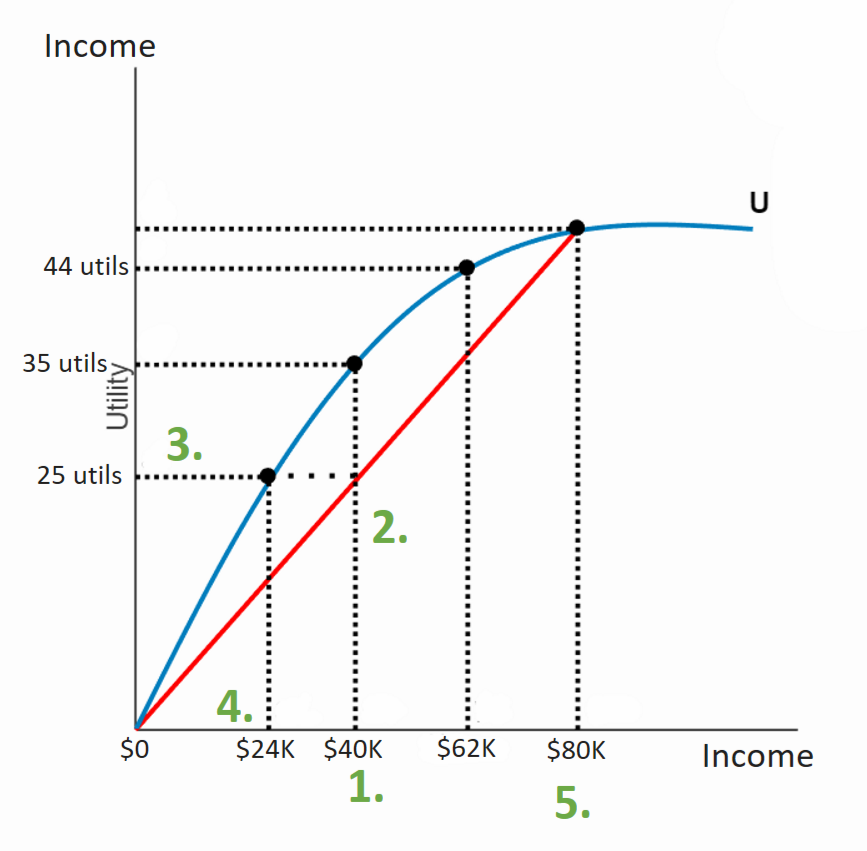

✏ Aga usually has an income of $80K, but there is a 50% chance that she will lose it all. The diagram below illustrates her utility function.

A✏ Calculate the EV of her income.

B✏ Calculate her EU

C✏ What is her CE?

D✏ What is the max premium she would pay to guarantee an income of $80K.

We will use the following steps to answer all four questions at once!

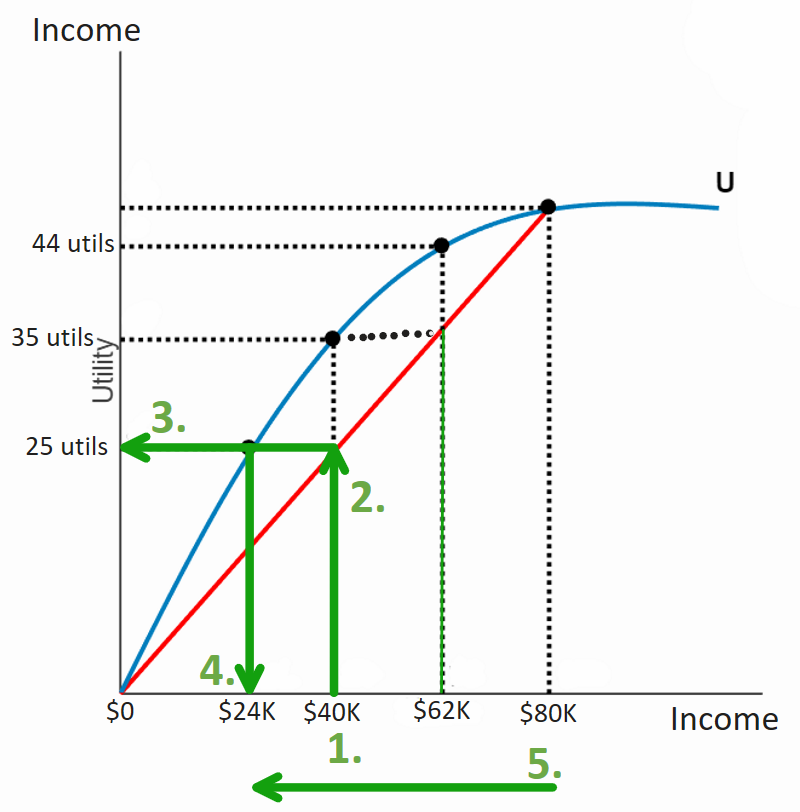

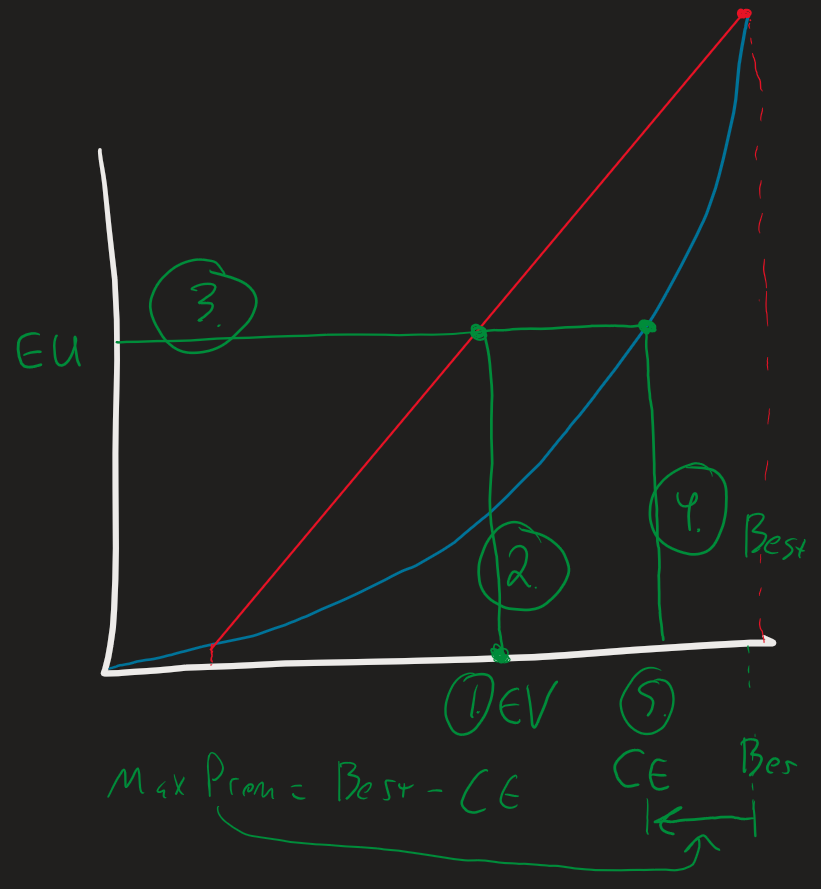

Shortest version (there is a diagram for this at the bottom)

1. Calculate the EV.

2. Draw line Up from EV to the straight line to get the point that represents their gamble (point in middle of the straight line)

3. Draw line Over from that point to Y axis to get the EU.

4. Draw line Down from where you crossed curved line to get the CE ($24K)

5. Premium

The steps are illustrated, below:

Now we apply the five steps:

A✏ Calculate the EV of her income.

B✏ Calculate her EU

Follow steps 2 and 3, drawing a line up from $40K and over from the orange point to get that the EU of 25 utils.

C✏ What is her CE?

Draw a line down from the curved line to get the . It turns out, according to the graph, that $24K for sure also gives her 25 utils!!

Therefore, $24K, for sure, is equivalent to her current gamble. It is her “Certainty Equivalent” to her current gamble.

D✏ What is the max premium she would pay?

The max premium she would pay will be . If she pays this and is fully ensured, she is guaranteed of having $24K, which is her certainty equivalent.

Note: The numbers that we get in this problem are will feel strange because we are assuming that Aga is highly risk averse and that she faces an extremely large risk of financial ruin. If the risk of financial ruin were lower and she were less risk averse, the number for the premium would feel more realistic.

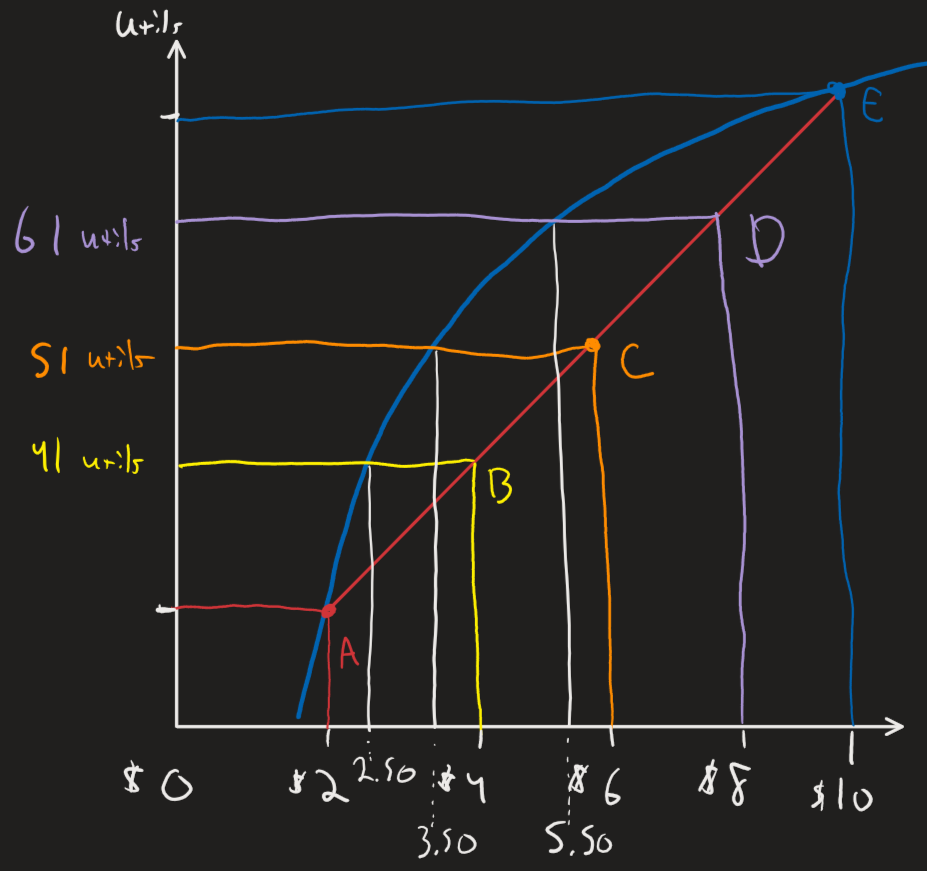

With different numbers

Section titled “With different numbers”

Aga usually has an income of $10K, but there is a 50% chance that she will lose all but $2K of it. The above diagram illustrates her utility function. What is the EV of her income, her EU without insurance, her CE, and the max premium she would pay?

To solve this, you must follow these steps:

A✏ Calculate the EV of her income.

B✏ Calculate her EU

Without insurance, her EU is 51 utils.

C✏ What is her CE?

It turns out, according to the graph, that $3.50 for sure also gives her 51 utils!!

Therefore, $3.50, for sure, is equivalent to her current gamble. It is her “Certainty Equivalent” to her current gamble.

D✏ What is the max premium she would pay.

The max premium she would pay will be . If she pays this and is fully ensured, she is guaranteed of having $3.50, which is her certainty equivalent.

Aga usually has an income of $10K, but there is a 25% chance that she will lose all but $2K of it. The above diagram illustrates her utility function. What is the EV of her income, her EU without insurance, her CE, and the max premium she would pay?

A✏ Calculate the EV of her income.

B✏ Calculate her EU

We go up to the red line and over to evaluate a gamble. .

C✏ What is her CE?

$5.50 will also give her 61 utils, based on the blue line for certain outcomes.

D✏ What is the max premium she would pay.

If she pays $4.50 and is guaranteed an income of $10, then she is left with $5.5, which is equivalent to being uninsured, so she would be willing to purchase the insurance.

If insurance is offered for less than $4.50, she will purchase it with enthusiasm and be glad she could buy it.

If insurance is offered for more than $4.50, she will reject it.

At a price of $4.50, she is completely indifferent between purchasing it or not purchasing it.

(Often, if someone is indifferent, in a question like this, we will assume that they purchase.)

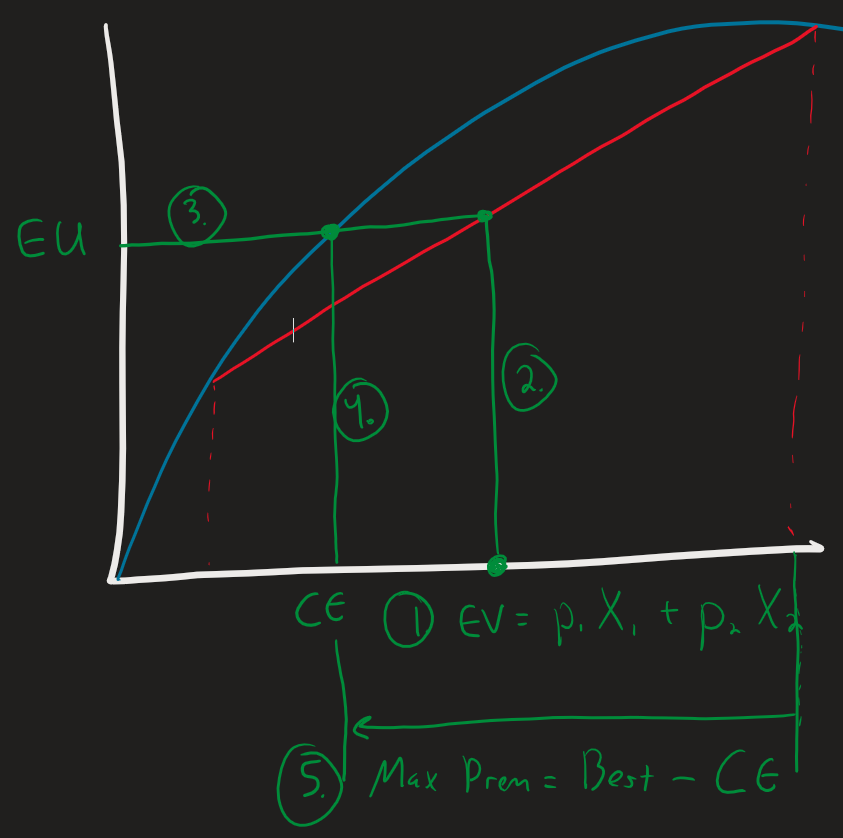

Below, please find a diagram that illustrates the following five steps.

Shortest version

1. Calculate the EV.

2. Draw line Up from EV to the straight line to get the point that represents their gamble (point in middle of the straight line)

3. Draw line Over from that point to Y axis to get the EU.

4. Draw line Down from where you crossed curved line to get the CE ($24K)

5. Premium

The following two diagrams illustrate how all five steps play out with both a risk-averse and a risk-loving individual.

Risk averse:

Risk loving:

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.