👨🏫 Notes on E-1000 Lecture 1

The Central Questions of Economics

- What gets produced? (firms choose quantities or shut down, etc.)

- How does it get produced?

- Who gets what is produced? (demand) In other words, how does a society deal with scarcity?

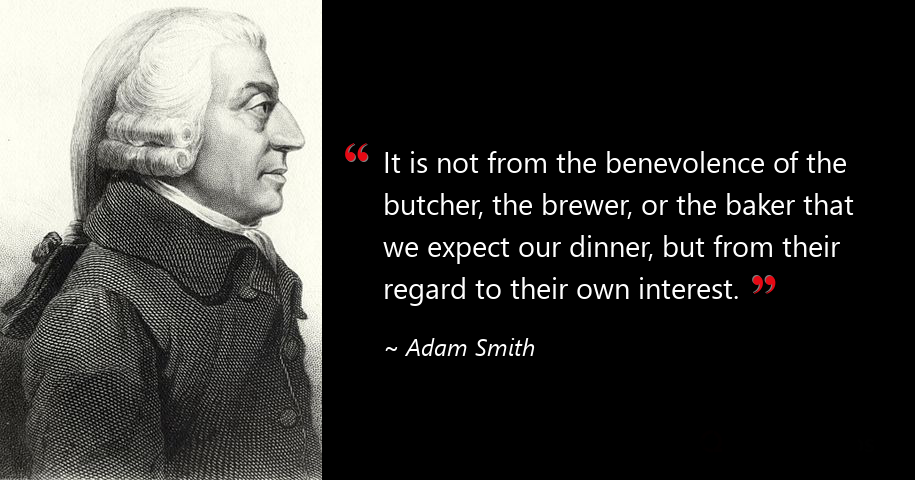

The Essence of a Market System:

Self-interest, checked by competition, within a framework of law

Four Central Concepts of Economics

- People are Rational

- People Respond to Incentives

- Every Decision Involves an Opportunity Cost

- An opportunity cost is “everything that you give up” when choosing an option.

- The Best Decisions are Made by Thinking “at the Margin”

- To decide how much to produce, just compare Marginal Revenue vs. Marginal Cost

- Produce whenever MR≥MC

Microeconomics - studies decisions of individual consumers (D), firms (S), and markets

Macroeconomics - studies entire economies/country all at once (unemployment rate, GDP, inflation, etc.)

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.