👨🏫 Notes on Lecture 4

Pindyck and Rubinfeld: Sections 5.1 – 5.2

- Read second subsection in section 5.3, which covers “Insurance.” It is pp. 171-173 in the 8th ed and the MyLab Ebook. It is pp. 169-172 in the 9th ed.

Basic Definitions

Section titled “Basic Definitions”Expected Value (EV)

= Probability of Outcome 1 × Value of Outcome 1

+ Probability of Outcome 2 × Value of Outcome 2

+ Probability of Outcome 3 × Value of Outcome 3

+ …

+ Probability of Outcome N × Value of Outcome N

EV is used to measure the cost of providing insurance.

It’s also used by quantitative hedge funds and professional gamblers

EV Example: Two Possible Summer Jobs Option I: Work on the Local Newspaper:

- Pays $2,000 for sure

- EV(Option I) = 1 × $2,000 = $2,000

- (“for sure” = 100% probability)

Option II: Internet start-up

- 50% chance of making $1,000

- 50% chance of making $4,000

- EV(Option II)

- = .5 × ($1,000) + .5 × ($4,000)

- = $2,500

Expected Utility (EU)

= Probability of Outcome 1 × Utility from Outcome 1

+ Probability of Outcome 2 × Utility from Outcome 2

+ Probability of Outcome 3 × Utility from Outcome 3

+ …

+ Probability of Outcome N × Utility from Outcome N

Returning to Summer Job example:

EU(Option I) = 100% × U($2,000) = U($2,000)

EU(Option II)

= 50% × U($1,000) + 50% × U($4,000)

People and firms always select the option with the highest EU.

Expected Value is used by insurance companies to estimate their costs. The people who do these calculations to calculate the “loss ratio” are known as actuaries. EV is helpful to insurance companies because of something called the law of large numbers.

EV doesn’t explain many of our decisions very well. EU does much better and is used in almost all economic theory. In economic theory, we calculate the expected utility of all of the options that the person is facing. Expected utility theory says that if they are rational, they will choose the option with the highest expected utility.

The utility function and risk attitudes

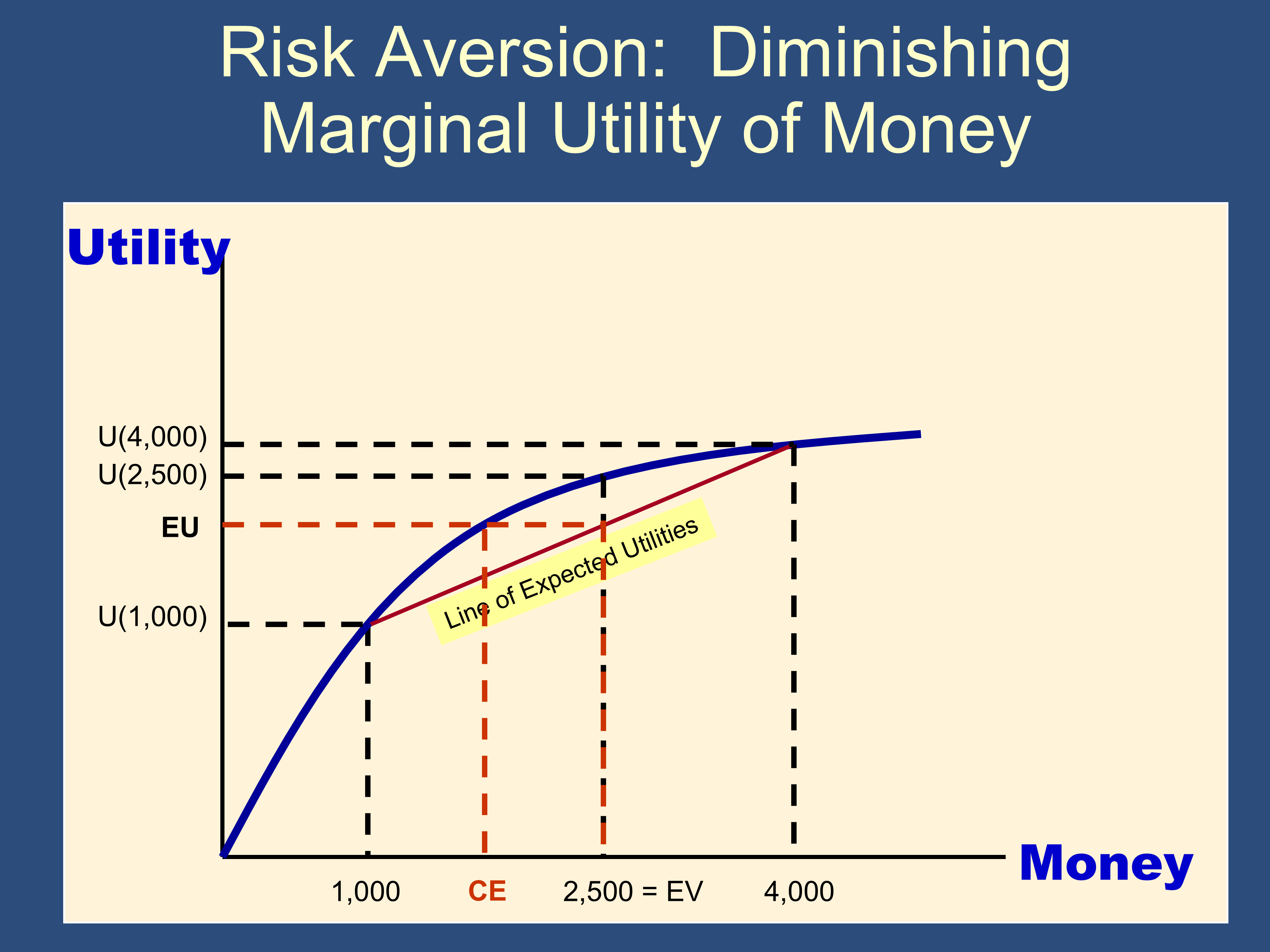

Section titled “The utility function and risk attitudes”Marginal utility = slope of utility curve

Risk Averse ⇨ Diminishing Marginal Utility of Money ⇨ Diminishing Slope of Utility Curve (gets flatter)

Risk Averse: CE < EV

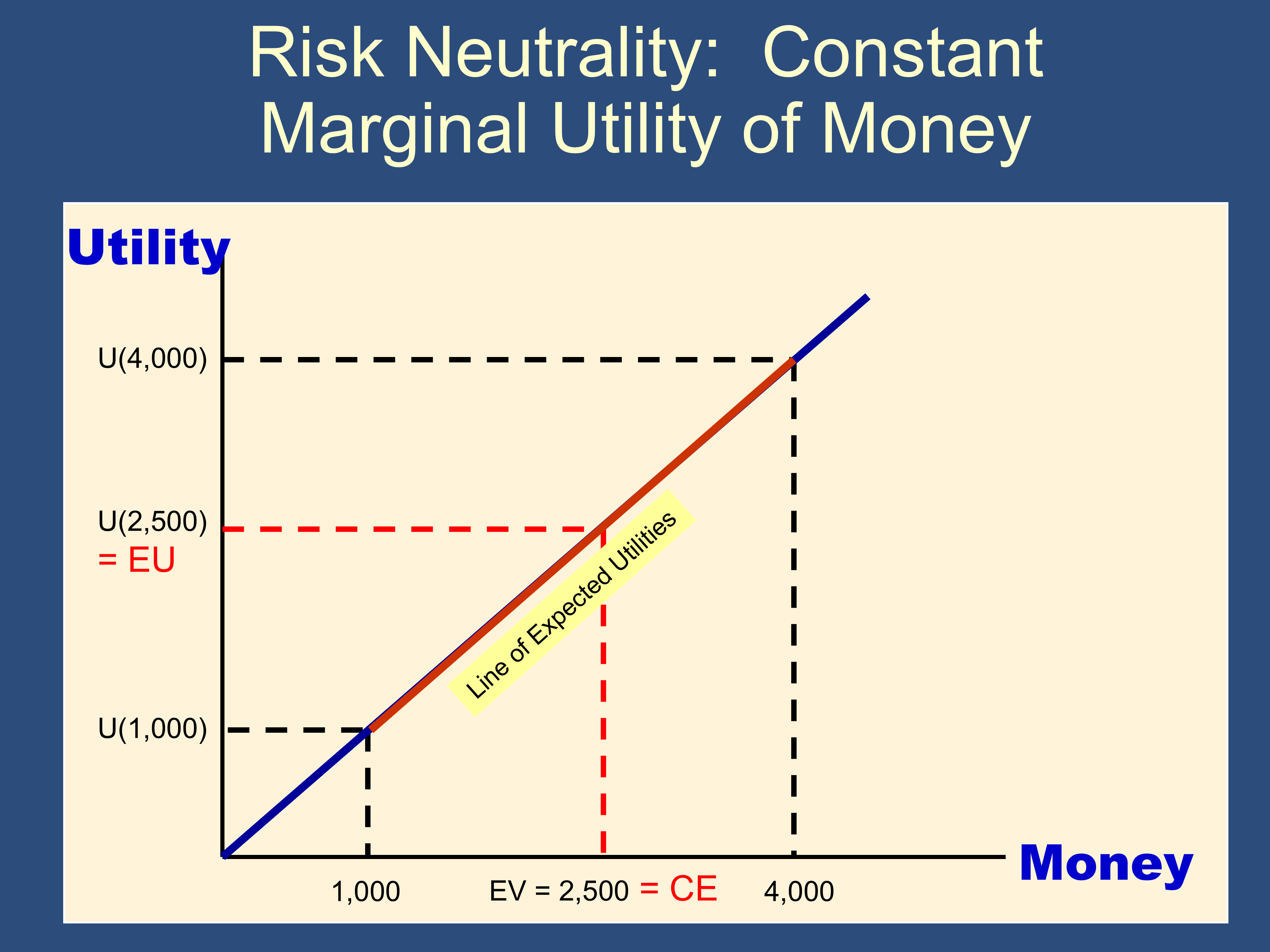

Risk Neutral ⇨ Constant Marginal Utility of Money ⇨ Constant Slope of Utility curve (straight)

Risk Neutral: CE = EV

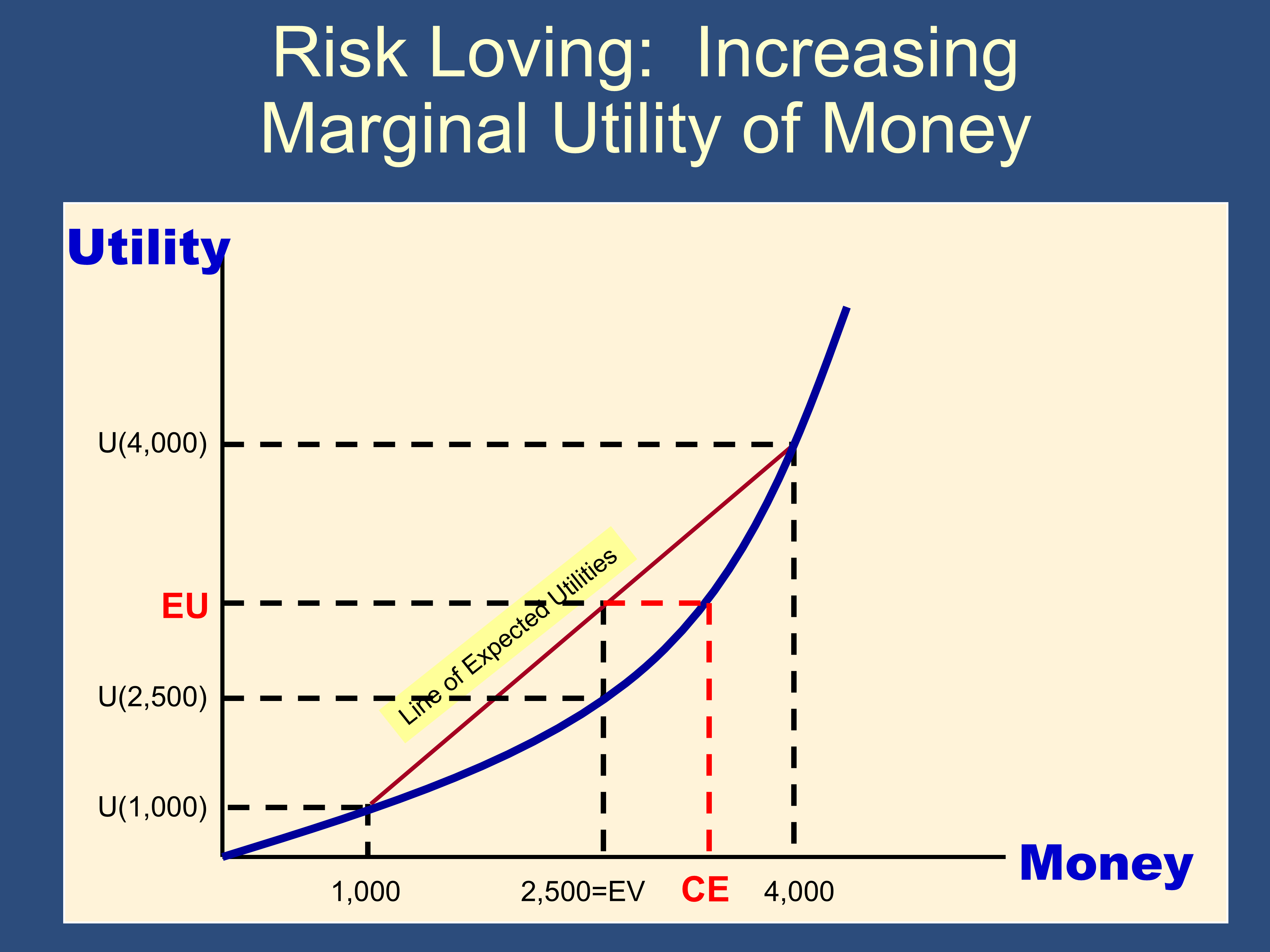

Risk Loving ⇨ Increasing Marginal Utility of Money ⇨ Increasing Slope of Utility Curve (gets steeper)

Risk Loving: CE > EV

Risk attitudes and fair/winning/losing bets

Section titled “Risk attitudes and fair/winning/losing bets”Suppose your net worth is $200K and I offer you a bet. You can provide a fair coin (I’ll test it to ensure fairness). We’ll flip it fairly. If you win the coin toss, I give you $220K. If you lose the coin toss, you give me $200K.

The EV of this gamble is 50%×$220,000 + 50%×(-$200,000) = $10,000

But a typical person is risk averse and wouldn’t accept the bet.

Background:

- If a bet has an EV of 0, it is a “fair bet”

- If a bet has an EV > 0, it is a “winning bet”

- If a bet has an EV < 0, it is a “losing bet.”

If an expected utility maximizer is offered a winning bet, like the one above, and they reject it, it is because they are risk averse in the relevant portion of their utility function.

If someone is offered a losing bet, and they accept it, they are probably risk loving.

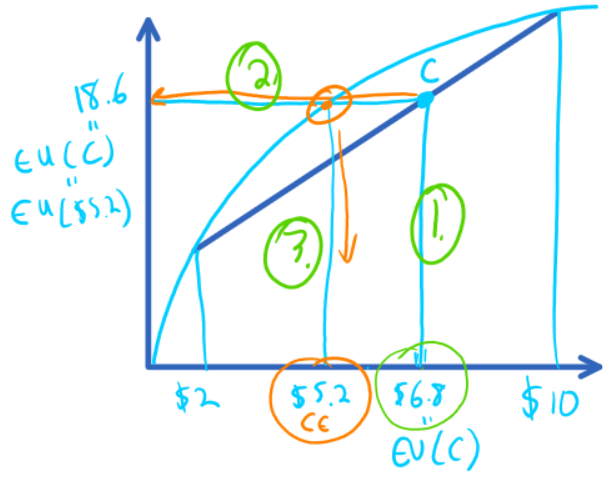

How to analyze a problem

Section titled “How to analyze a problem”

The darker blue line is the line of expected utilities. It shows the EU (and EV) from all bets where you either get $2 or $10.

Point A means you have a 100% chance of getting $2.

For any point on the line of EU, if you draw a line down, you get the EV ($6.8). If you draw a line to the left, you get the EU (18.6 utils).

This is the picture for certainty equivalents.

- Find the point that represents the gamble the customer is facing. (point C).

- Draw a line to the left to find the EU of that gamble. (18.6) Draw it from the straight line of EUs.

- The curved line represents the “Certain bets.” Where it hits the horizontal line is the Certainty equivalent

The CE is drawn down to the X Axis using the Utility Function, not the Line of EU.

- The utility of bet C is 18.6 utils. The utility of getting $5.2 for certain is 18.6 utils.

Therefore they are equivalent and $5.2 is the Certainty Equivalent of bet C.

- Practically, on a problem diagram, you will often calculate the EV and draw a line up from it (line 1). This helps you find the EU of the gamble the person if facing.

- Then you want to figure out the EU, so you draw a horizontal line over to the Y axis (line 2)

- Wherever line 2 hits the utility function, you draw a line down to find the CE (line 3)

- To find the maximum premium, just “clean them out.” Find the difference between their guaranteed income ($10) and their CE ($5.2). ($10-$5.2=$4.8)

✏️ The following represents Jeff’s utility for income.

| Income | Utilities |

|---|---|

| $20K | 10 utils |

| $40K | 80 utils |

| $60K | 130 utils |

| $80K | 150 utils |

Jeff can choose between a job that guarantees him $60K or a riskier job with a 70% chance of earning $80K and a 30% chance of earning $20K. Which should he take?

✔ Click here to view answer

Sure thing: EU = 100%×130 utils = 130 utils

Riskier job: EU = 30%×10 utils + 70%×150 utils = 108 utils

He should choose the safer job.

✏️ What is Jeff’s CE of a job that has a 50% chance of $80K and a 50% chance of $20K?

✔ Click here to view answer

First let’s calculate the EU of the bet: 50%×10 + 50%×150 = 80 utils

Is there a certain income that gives him 80 utils? Yes! If he has an income of $40K, he has an EU of 100%×80utils = 80 utils. With an income of $40K, he has an EU of 100%×80 utils = 80 utils, so $40K is his CE.

✏️ Suppose Jeff has the 50-50 job mentioned above. What is the maximum premium he would pay to be guaranteed of getting the full $80K?

✔ Click here to view answer

With this insurance, he will be left with $80K - premium. If the premium is maximized, if you charge him $.01 more, he wouldn’t take it. In other words, with a maximal premium, the EU of the insurance and no insurance are the same.

We must “clean him out” so he is left with his CE amount. If we leave him with his CE, that will be “equivalent” to no insurance, so he might purchase the insurance. Bottom line, he will have $80K - Premium, and that must leave him with the CE.

$80K - Premium = CE (equally happy either way)

Premium = $80K - CE = $80K - $40K = $40K

The maximum premium he would theoretically pay is $40K.

Max premium = best outcome - CE

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.