✏ L4 Practice - Expected Utility

✏ Evgenia lives in near a fault line. Her total wealth next year, including her house, will be $500,000.

However there is a 10-percent chance that a big earthquake will occur next year and destroy her house, valued at $200,000. What is Evgenia’s expected wealth next year if she chooses not to purchase insurance?

✔ Click here to view answer

The probability of no earthquake is

Setup:

| Outcomes | Probability | Wealth |

|---|---|---|

| No earthquake | 90% | $500,000 |

| Earthquake | 10% |

✅

✏ Evgenia’s utility for various levels of wealth is shown below. What is her Expected Utility if she chooses not to purchase insurance?

| Wealth | Utility |

|---|---|

| $200,000 | 447 |

| $300,000 | 548 |

| $400,000 | 632 |

| $450,000 | 671 |

| $500,000 | 707 |

| $600,000 | 775 |

✔ Click here to view answer

✅

✏ Suppose that she can purchase insurance for $50,000, which will completely fix/replace her house if there is an earthquake (it will be worth $200K again). What will her utility be if she purchases the insurance? Will she purchase it?

✔ Click here to view answer

If she purchases insurance, then her outcomes are as follows:

| Outcomes | Probability | Wealth |

|---|---|---|

| No earthquake | 90% | |

| Earthquake | 10% |

long way to calculate EU:

Oh, wait, she just has a 100% chance of having a wealth of $450.

Evgenia will not purchase the insurance. We calculated above that if she purchases it, her EU is 671, but if she doesn’t purchase it, her EU is 691.1 ✅

✏ It turns out that Evgenia’s certainty equivalent is 477,619. What is the maximum that she would pay for insurance?

Note: CE = 477,619 and EV = 480,000. This illustrates that for people who are risk averse. She is very slightly risk averse.

✔ Click here to view answer

The insurance will guarantee her that her wealth is $500,000 - premium. She’ll only purchase the insurance if her wealth is at least her CE (otherwise, she’d be less happy than if she hadn’t purchased the insurance.)

In other words, she will purchase if:

final wealth with insurance ≥ her certainty equivalent

✅

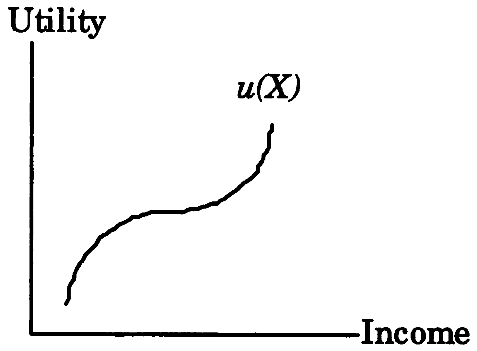

✏ Immanuel’s utility function is show below. Is he risk loving, risk averse, risk neutral, or some combination? If a combination, at which levels of income, relatively speaking, does he exhibit each tendency?

✔ Click here to view answer

Immanuel is risk averse at low levels of income, as indicated by the fact that his utility curve gets flatter and almost beings to slope down. Immanuel is risk loving at higher levels of income, as indicated by the fact that his utility curve gets steeper and almost becomes vertical. ✅

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.