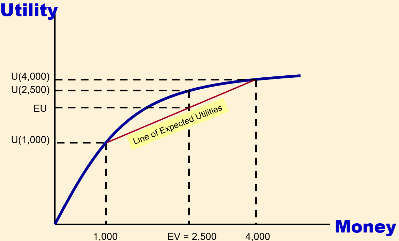

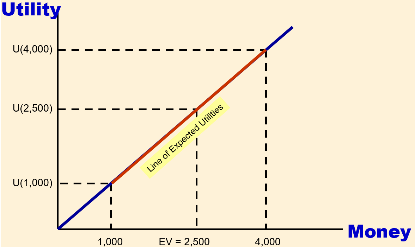

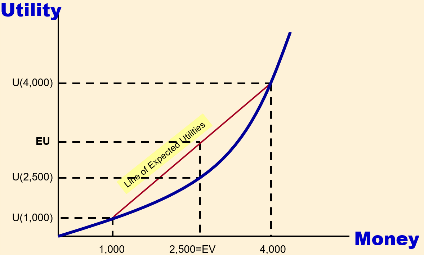

🔎 Attitudes toward risk

| Risk Averse | Risk Neutral | Risk Loving | |

|---|---|---|---|

| Who? | Most people | * | Crazy |

| MU | Decreasing | Constant | Increasing |

| Shape |  |  |  |

| CE vs EV |

* Insurance companies, high frequency professional traders, and professional gamblers are slightly risk averse, but almost risk neutral

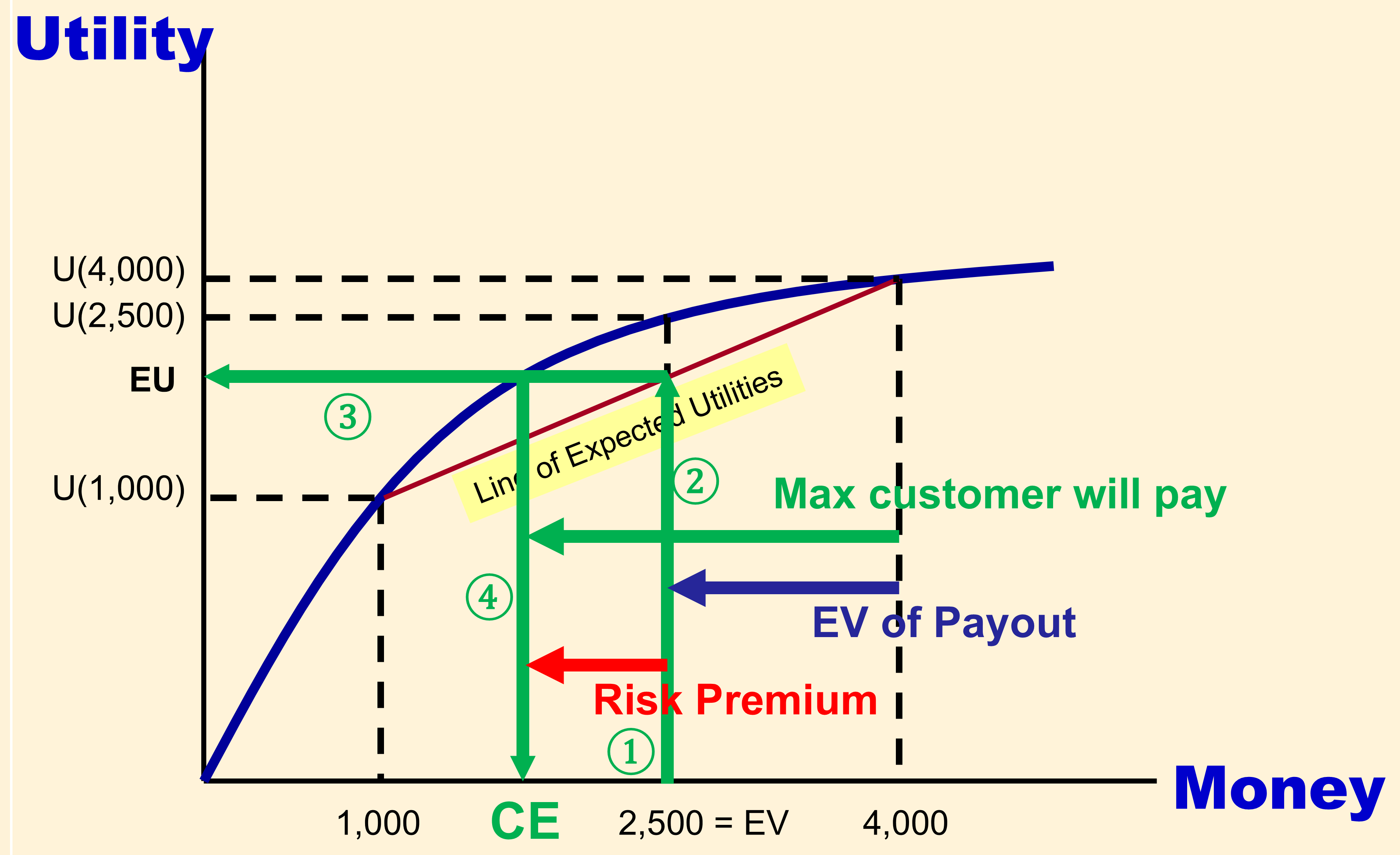

Insurance companies, as described above, tend toward risk neutrality. It is rational for them to do so because of the law of averages. If you take a large number of small bets and you evaluate each bet in a risk neutral way, then in the long run, you’ll tend to make money. They evaluate their costs, as described earlier, using EV. The EV providing an insurance policy is known as the “actuarially fair” premium for the policy.

Sidebar ( YOU ARE NOT RESPONSIBLE FOR THIS, BUT IT IS IN THE BOOK)

Is this person willing to pay more or less than the actuarially fair amount for their insurance policy?

The person is willing to pay .

It costs to provide the insurance.

Because , the person is willing to pay a premium, above the actuarially fair amount for their insurance.

Because their willingness comes from risk aversion, we refer to this extra amount that they will pay as their risk premium.

We can calculate the risk premium as

The fact that people in general are risk averse implies that they will pay a positive risk premium for insurance. Because the Actuarially fair amount is how much it costs to provide insurance, this means that insurance companies can provide insurance profitably to risk averse people.

Payout is .

EV of payout is

See also: 📖 Textbook on Insurance

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.