📰 Asymmetric information with executing stock trades

Unless you love finance, you may want to skip this example, as it is rather wonky. If you do like finance and are curious, please ask me about this article!

From the article, M-ELO (Still) Has the Best Markouts

Section titled “From the article, M-ELO (Still) Has the Best Markouts”Many investors have a long-term outlook as well as a unique, slow alpha trading signal. If that’s the case, trading costs can be minimized by slowly accumulating positions without signaling or holding up the market.

Although placing buy orders on the bid lets you capture a whole spread, it can also signal a trade to the market. For even more patient investors, a strategy that uses hidden orders like iceberg or midpoint orders can work better.

However, even though they are not advertised, many hidden orders are still “firm” at their hidden prices. That means they can still suffer from something traders call adverse selection (what others call getting “picked off”).

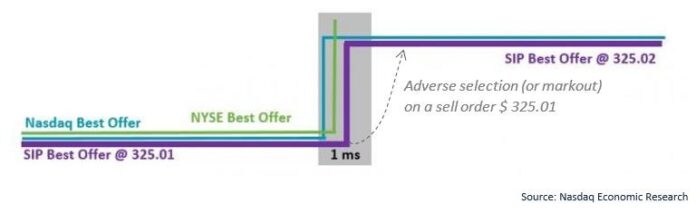

Adverse selection happens in less than a millisecond (ms)

Adverse selection occurs when you get a fill only to find out that it’s cheaper to trade at new prices than at the prices where you just traded. For example, consider an order resting on the offer in Chart 1 at $325.01. The trade that happened in the grey box would have filled your order, whether you were hidden or not. But an instant later, the new offer is at a price of $325.02, a better price to sell.

It’s a form of buyer’s remorse, where if only you’d waited a bit longer, you could have sold at a better price. For a trader, it also requires perfect hindsight because trades can easily do the opposite and make your next trade more expensive too.

But there are ways to avoid adverse selection. To do it, you need to avoid being filled by large or “informed” spread-crossing trades.

Nasdaq’s Midpoint Extended Life Order (M-ELO) order type does just that. M-ELO orders all have to wait to activate, which means it will only trade with orders that have been resting at the same place for at least the same amount of time. Given urgent spread crossing orders don’t wait, they won’t interact with M-ELO. So using a M-ELO order makes it more likely you will find other longer-term traders who are also willing to join the market more patiently.

Read more:

https://www.tradersmagazine.com/departments/algos/m-elo-still-has-the-best-markouts/

https://www.nasdaq.com/articles/what-markouts-are-and-why-they-dont-always-matter-2020-07-23

Feedback? Email munger.e1010@gmail.com 📧. Be sure to mention the page you are responding to.